- Stock Exchanges in India are exploring the opportunity to venture beyond the current businesses to create data repository services, Artificial Intelligence or a big data analytics eco-system. Last week, the Bombay Stock Exchange and the National Stock Exchange sought Securities and Exchange Board of India (SEBI)’s permission to form a separate entity to take on these businesses. NDSL e-governance, Unique Identification Authority of India‘s Aadhaar data, and other related government projects are a gold mine of data and can propel these companies into the future of the Artificial Intelligence ecosystem.

- The latest LinkedIn survey of 2017 has proven that machine learning engineer, data scientist, and big data engineers have ranked among the top emerging jobs this year. According to the LinkedIn survey, the fastest growing job over the last five years is machine learning engineer, as the number of open positions on LinkedIn has multiplied by nearly over 10 times. The profile of a data scientist came in second, with the number of jobs growing 6.5 times since 2012. The study also said that the growth and widespread application of more sophisticated technology such as artificial intelligence, more specialized machine learning and data-specific roles have emerged on top. The study went on to add that these jobs were also widely available outside the technology industry. While companies from all industries want machine learning engineers and data scientists, but LinkedIn’s data has found that there is not enough talent out there to fill the gap. The number of data scientist jobs has gone up by 650 percent since 2012, with there being more than 35,000 people in the US with relevant skills. But the LinkedIn reports says that this is nowhere near enough to satisfy demand at the moment.

- Key highlights of a report by UOB and E & Y titled State of Fintech in ASEAN

- The report states that ASEAN embodies the aspiration of 10 uniquely different countries in Asia to bring about greater economic prosperity, and social and cultural progress for the people of ASEAN. Countries such as Singapore and Thailand are already moving towards a common national payments infrastructure and QR code standard, which could become the payment standard for ASEAN in the future. Except for Singapore, 70 per cent of wage payments and government transfers within ASEAN are still received in the form of cash, giving rise to a prime opportunity for digital wallets to thrive. Indonesia and Malaysia are already moving in this direction with more than 146 payment Fintechs being created, and this number is set to grow.

- In ASEAN, peer-to-peer (P2P) lending is forecast by Allied Market Research to grow at a compound annual growth rate of 51.5 per cent to 2022. Indonesia, Malaysia and Singapore have clear regulations on P2P lending, which have encouraged the setting up of more than 40 P2P lenders in the past two years. Thailand has issued a consultation paper, whereas the Philippines and Vietnam are still at the nascent stage with few players currently operating locally. The speed of FinTech adoption across ASEAN is varied, but the momentum is building.

- ASEAN as an engine of economic growth and prosperity has caught the eye of global investors and there is an abundant supply of early-stage funding in the region. Investment in Southeast Asia Fintechs jumped 33 per cent year-on-year to US$252 million in 2016, according to Tracxn. Total investment in the region this year is poised to exceed US$338 million. Beyond the traditional forms of funding from angel investors and venture capitalists (VCs), crowd funding, venture debt and bank venture funds have also contributed to the rise in dry powder available for investing in ASEAN Fintechs. While Fintechs are still in their early stage in ASEAN, digital platforms such as e-commerce have proliferated, backed by internet giants who have the financial muscle to make large, billion dollar investments in the next unicorns of ASEAN. The battle for the consumer wallet and mindshare will continue to drive investment as internet giants seek to establish a foothold in ASEAN, starting in Singapore, Indonesia and Thailand.

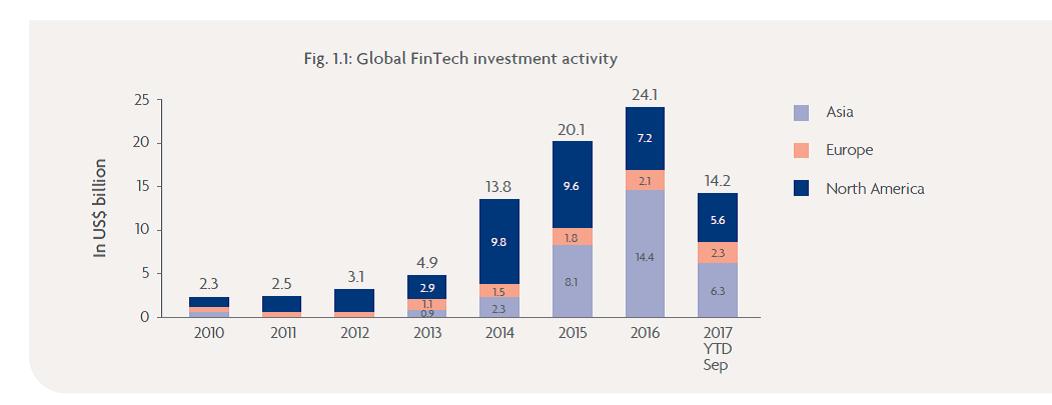

- The global FinTech industry attracted more than US$24 billion in investment in 2016, ten times the level received in 2010. FinTech investment in Asia exceeded North America for the first time in 2016, led by blockbuster deals. In China, including Alipay and Lu.com raising US$4.5 billion and US$1.2 billion respectively. ASEAN too is witnessing visible growth in FinTech. In 2016, investments in the Southeast Asian FinTech market increased to US$252 million, compared with US$190 million in 2015, a rise of about 33 per cent. Total investment up to September 2017 has already exceeded that of 2016 to reach US$338 million . Most of the funding in the region is from seed and angel investors.

- Strong GDP growth, favourable demographics, digital readiness and regulatory initiatives offer a plethora of opportunities for Fintechs across the ASEAN region. Improved cross-border interoperability and policy standardisation will also help ASEAN to maximise the full benefits of digital technology.

- Most ASEAN countries have already identified FinTech as a major growth area and have taken steps to nurture a supportive environment for FinTechs to prosper. Singapore is the market leader in ASEAN with the Monetary Authority of Singapore (MAS) taking a number of steps to promote FinTech. Backed by a supportive regulatory regime and progressive policy initiatives, Singapore stands competitively among global FinTech hubs. Other ASEAN countries have been quick to follow suit, though their priorities and approaches are different. Most of the regulators are taking steps to facilitate innovation to ensure economies reap the benefit of innovation and remain competitive. At the same time, regulators are ensuring that they protect the integrity of the local financial services markets.

- ASEAN holds promise for Fintechs, underpinned by unmet demand for financial services from the unbanked and underbanked. Regional banks, regulators, policymakers and academia have acknowledged the need for innovation. and are taking steps to create an inclusive ecosystem. If the technology talent puzzle is also solved, ASEAN will be able to leap forward with FinTech – and enter the new economy as a key player in the global arena.

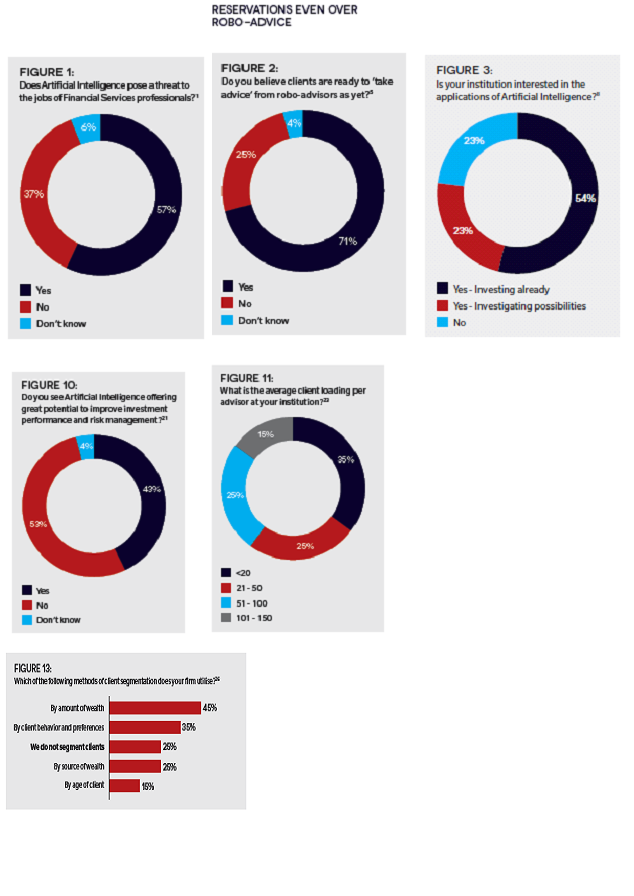

- Summary of a report Applying Artificial Intelligence in Wealth Management by Wealth Briefing, E & Y and Finantix:

- The aim of this report is to cut through the hype & confusion around AI and to outline compelling use cases for the technology across the client life cycle. It gives clear examples of what the technology might look like “in action” when tackling pain points that most wealth managers will be all too familiar with. The report thus covers ways in which AI can be leveraged to generate leads and then engage more effectively with those prospective clients; how due diligence can be made more thorough and efficient; and where technology can help deliver truly holistic wealth management solutions and relationships that feel more personalised without further burdening personnel.

- The report also tackles some of the broader strategic issues AI can also assist with, such as improving data management and making sophisticated client segmentation techniques a reality. In mapping AI applications to the client life cycle in this way, we hope to point a workable way forward with this very exciting, but still quite nascent technology. AI might be only just coming to the fore, but wealth managers should be under no allusions as to how fast things are developing, however.

- One of the key messages is that AI is far from being “still in the lab”. A multitude of both private and public sector organisations have already adopted the technology, and we can expect its potential to grow exponentially with rising acceptance among consumers. As ever, retail institutions are leading the way due to their larger technology budgets and economies of scale. Banks and insurers are already deploying tools like “cognitive agents” to great effect and using AI data analyses to massively increase efficiencies while also reducing risk.

- Forward thinking private banks and wealth managers will surely follow close behind. More than anything else, however, we hope to convince professionals that AI should be embraced as a facilitator, rather than feared as a devourer of jobs. Nor should it been seen as something that will erode the personal relationships at the heart of the wealth management proposition and all the eminently human skills advisors bring to bear. As one of our contributors so elegantly put it, “we should be thinking about AI in terms of Iron Man, rather than the Terminator”. We look forward to tracing the upwards trajectory of AI across the wealth management industry, and hope it rapidly relieves some of the many pressures on the industry.

- Key points covered in the report are – a) The real role of AI and why wealth managers have less to fear than they might think b) Leveraging AI for lead generation and management c) Effective engagement to improve client win-rates Rating kyc: faster, deeper client due diligence d) Holistic financial planning and customised portfolios e) Personalised relationships without overburdening personnel f) Making sophisticated segmentation a (profitable) reality g) The regulatory implications of using AI and how legislation is developing