Credit Risk Analytics: Macroeconomic modelling for Bank for PD impact

Background

One of the Banks wanted to predict the impact of Covid scenario on futuristic PIT Probability of Defaults (PD) for their portfolio considering the current environment for this year and subsequent years. The Bank is one of the leading Private sector Islamic bank in Middle East Asia. They have a large Lending portfolio comprising retail and Corporate customers.

Approach

We took Macroeconomic factors like GDP growth rate, Inflation, crude oil price and Government spending for the prediction of PDs. We checked for autocorrelation between all the macro factors and removed the variables with correlation greater than 90%. After testing collinearity we performed log transformation to get normalised data and then standardised the factors to perform further modeling. It required linking of historic PDs (quarterly) for each risk Transition PD buckets through Principal Component Analysis and Logistic regression. In PCA each principal component is a linear combination of underlying variables. Each principal component is uncorrelated with other components. This process is called dimensionality reduction and is used to avoid multi-co-linearity problems and is easier to project PC’s as they are uncorrelated.

Illustration of PCA

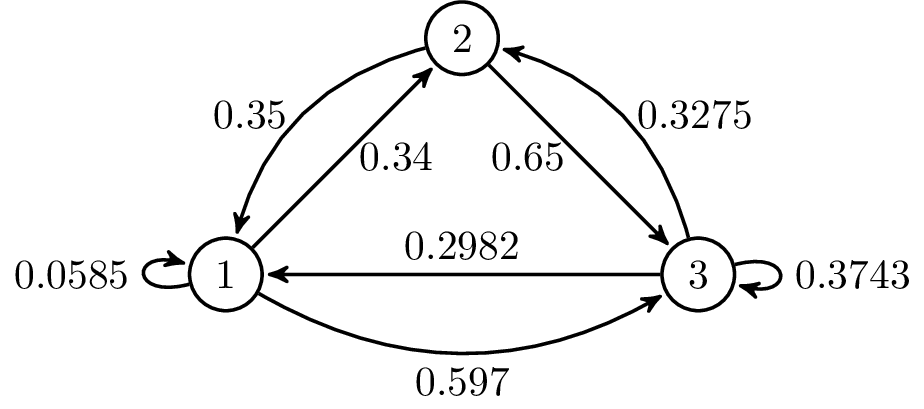

The quarterly projections were later on converted to annual average values on which Markov Chain was applied to get the cumulative annual transition PD buckets. The Markov chain is used for projecting future state probabilities using Transition PDs.

Illustration of Markov Chain

We projected macro-factors using economist forecasts and statistical modeling. The U-shaped and V-shaped recovery over the next five years had to be factored in. Once the factors are projected we converted the factors into PDs.

Solution

We provided the projected quarterly PD buckets along with cumulative transition metrics. Using the model and macro-economic projections, we projected forward looking segment wise defaults and PIT PDs. We projected PDs product-wise and Rating/Bucket-wise. The PDs are being used by the bank for their analysis and IFRS accounting